Adam Śmietanka | CASE Economist

The topic of the VAT compliance has gained a particular significance in the recent years in Poland. It has become a part of a recurrent, heated political debate and has been often used instrumentally by politicians and experts alike. However, a growing interest in the forgone VAT revenues is not just limited to Poland. Thus, as the estimation techniques and underlying data on VAT components have been improving, Poland and many other countries in the EU have seized the opportunity to scrutinise national VAT Gaps and estimate their size using various techniques.

This article discusses observations for Poland based on the results and experience gained from estimating and evaluating the VAT Gap in all EU Member States. These conclusions relate to both the past and the future. Firstly, we summarise basic information on the topic, specifically in the historical context of the public finance in Poland. Second, we show what lessons from the past could be drawn for foresighting dynamics of the VAT Gap, especially in the context of the COVID-19 pandemic.

What exactly is the VAT Gap?

Since 2013, every year CASE has been estimating the size of VAT Gap of the EU countries under the request of the European Commission. A standardised methodology based on Own Resource Statements compiled at national level and over 500 observations for 28 countries over 18 years allowed us to develop an econometric methodology for studying VAT Gap determinants. Our econometric model explains the nature of the relationship between VAT Gap size and other variables identified as most relevant to the problem (for the details, see the section on Future Obstacles).

When studying the VAT Gap, it is crucial to understand its components. The simplest definition of the VAT Gap is the difference between the theoretical value of the VAT liabilities and the value of real VAT inflows. Usually, the VAT Gap is presented in relative terms — as a share of that difference in total VAT liabilities. The reasons for non-compliance are manifold, from fraud and criminal activity, through grey economy and tax avoidance, to tax optimisation and natural bankruptcies. All of those are heavily interconnected with formal and informal institutions and economic conditions and thus it is hard to find a tool which would be universally effective in the fight against the VAT non-compliance.

More than a theory

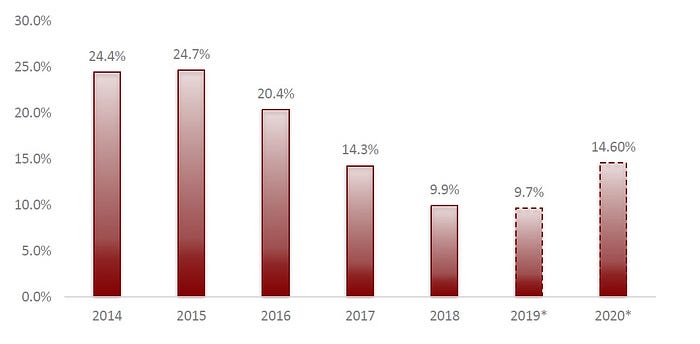

Reduction of the VAT Gap size has become one of the main goals for the currently ruling party in Poland (Law and Justice, PiS) since it assumed power in 2015, which created an awareness on the topic among the broader audience in the country. The increase of VAT revenues was to be a crucial source for financing of additional budgetary expenses, particularly flagships social programs of the ruling party (e.g. Family 500 plus programme). In 2016, the then Minister of Finance, Paweł Szałamacha, outlined a goal to reduce the VAT Gap from 24% to around 15% in three years. Indeed, the VAT Gap decreased substantially starting with a 4.3 pp drop in 2016 and 6.1 pp and 4.3 pp drops through 2017 and 2018, respectively. This was presented as a direct result of the government actions against VAT avoidance and the so-called “VAT mafia”, which fuelled further public debate on who and what can be credited with those successes.

The success led to the belief that this trend will continue into the future to the extent that it was included into Multiannual State Financial Plan for 2019–2022, which outlined the long-term fiscal strategy of the Polish government. The plan thus assumed extra PLN 8 billion of VAT revenue in 2020 due solely to the increased VAT compliance. Already by the end of 2018, some independent experts were sceptical about the potential to close the gap further, suggesting that most of the ‘easy’ sources of increasing compliance were already depleted. According to some of those experts, including CASE, the remaining potential for sealing the VAT Gap is more dispersed now and close to the size of the grey economy itself. Further actions to fight VAT non-compliance, therefore, would have to be a part of a broader, more comprehensive strategy in order to bring it down considerably.

Table 1. Year-on-year change in VAT revenue and its components in Poland (2016–2018)

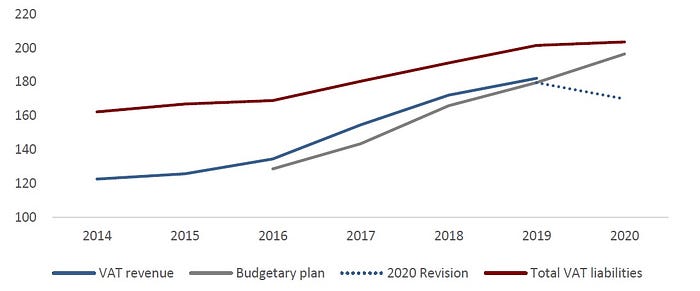

The Budgetary Act for 2019 assumed a 7.3% increase in VAT revenues compared to 2018. Although in terms of nominal revenues the plan was met, due to an upward revision of 2018 revenue figures the actual increase in the revenue was somewhat lower — 5.8%. This might still seem like a lot, but that increase was achieved almost exclusively through the growth of liability base, rather than as a result of increased tax compliance. Preliminary data suggests that in 2019 the VAT Gap fell only slightly, accounting for 9.7% of total liabilities, compared to 9.9% in 2018.

The plan to further decrease the Polish VAT Gap became even more important in the context of the 2019–2020 election season. One of the main points on the government agenda was a further extension of social transfer programs (e.g. fourteenth pension for each retired person) with the maintenance of a balanced budget for the first time in 30 years. As such the Budgetary Act for 2020 was even more ambitious — VAT revenues were planned to reach PLN 196.5 billion (already after a downward revision) — a 7.9% increase from 2019 figures.

Future obstacles

With the COVID-19 crisis that reached Poland in spring and a subsequent lockdown of a large part of the economy, quickly enough it became clear that the above-mentioned ambitious goals will not be possible to achieve. This can be explained not only by additional spendings within the Polish stimulus package worth PLN 115 billion (the so-called “anti-crisis shield”) but also by projected lower tax revenues for 2020.

In August, the government amended the Budgetary Act and cut VAT revenue projections by about PLN 25 billion. The new 2020 figures at around PLN 170 billion thus revert Polish VAT revenue to its 2018 levels. This correction was made assuming that private consumption will remain stable (or even grow slightly) in the year-on-year perspective, which suggests that the government is probably fully aware of the strong relationship between economic conditions and VAT compliance.

In the latest Report on the VAT Gap in the EU-28 Member States, CASE investigated this relationship thoroughly. A wide set of variables was tested for their correlation with the level of VAT compliance across all Member States throughout 18 years for which the VAT gap was calculated. Those variables could be grouped as follows: (1) tax policy indicators; (2) indicators of the macroeconomic situation; (3) indicators of institutional environment; and (4) proxies of VAT fraud. According to the model specification selected as best fitting during the analysis, the main determinants of the VAT gap are GDP growth, public deficit, IT expenditures in the area of tax administration, sectoral structure of the economy, and share of trade of products and services associated with the biggest risk of tax fraud. It is worth to mention that some factors (e.g. those related to the institutional environment, including trust in the system, harshness of tax authorities, etc.) are complex and difficult to measure thoroughly, hence have not been considered within the model.

Figure 1. Budgetary plans for annual VAT revenues and their execution, 2016–2020 (in billion PLN)

Figure 2. VAT Gap as a percent of total VAT liabilities in Poland

The selected model parameters and their significance prove how crucial macroeconomic conditions are for VAT compliance. In short, non-favourable economic situation adversely affects VAT revenues in two ways: through lower tax base and via a higher tendency for non-compliance of business entities. Taking advantage of the European Commission 2020 Spring macroeconomic forecast of the GDP and budget deficit, we were able to assess the nature and scale of impact that these factors might have on the Polish VAT Gap. Based on numbers provided by European Commission we estimate that the VAT Gap in 2020 will increase by almost 5 pp or to 14.6% of total VAT liabilities, which would mean a return to its 2017 level. Of course the crisis caused by coronavirus pandemic is exceptional and it is impossible to consider all the implications it will have — the model by its nature is based on historical data where the values of those macroeconomic variables were significantly different from those supplied for the purpose of forecasts.

Conclusions

This analysis shows the most probable scenario for public finance at this point and constrains it might face in the coming months and years.

Within those constraints, even stabilisation of the Polish VAT Gap at the level observed in recent years will be considered a success. In the upcoming years, the economic situation, and consequently, situation of the public finance, will surely largely depend on severity of the pandemic and level of governmental success in mitigating its adverse health and socio-economic impacts. Needless to say, budgetary planning must be based on realistic assumptions and take into consideration factors that are outside of government control — VAT collection is cyclical in nature and should be planned with long-term horizon in mind.